.svg)

.avif)

In the last post on Information Utilities, we spoke about the Information problem in the current insolvency process.

Let's do a quick recap:

Why Information Utilities are needed

The Insolvency and Bankruptcy Code (IBC) is an attempt to give creditors in India a fast, certain mechanism to enforce their debt claims.

One way the IBC tries to make the system faster is by removing the scope of evidence that can be used in an insolvency proceedings - confining the process as a verification to see whether there has been a default of debt.

Seeing whether a debt has been defaulted or not relies on 2 pieces of evidence - a) Debt Documentation and b) Debt Information

But in the conventional process there is an Information Problem that debtors exploit to cause delays.

The Information Problem consists of 4 vulnerabilities that are exploited by borrowers to cast doubt on the integrity and authenticity of debt information:

- Physically executed debt documentation is inherently prone to vulnerabilities of damage and mistakes

- The slow and inconvenient physical execution process incentivizes parties to take shortcuts - creating “chain of custody” vulnerabilities that cast doubt on the integrity of the documentation

- Physical documentation made it very hard to codify revisions and updates to the arrangements between a debtor and a creditor

- Debt information and documentation was fundamentally non-neutral. The creditor stores the original documents and maintains the information repository - which is inherently prone to mistrust and dispute

Debtors use these vulnerabilities to frustrate and delay proceedings before the NCLT. And delays - as we learnt in the last post - thwart the aims and objectives of the IBC process.

Information Utilities are designed to solve this problem - and ensure that the insolvency process is completed in a time-bound manner.

Enter Information Utilities

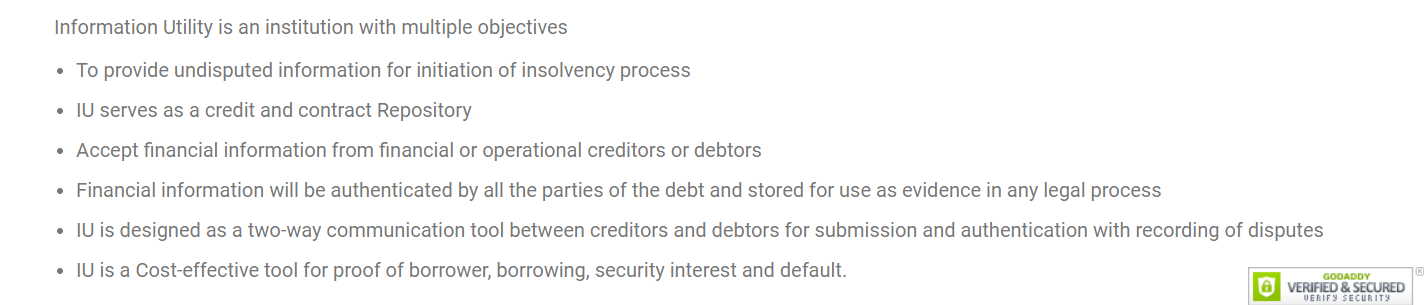

As per NeSL - India’s first information utility - an Information Utility is an institution with multiple objectives:

The first objective listed seems to lay down the overarching purpose of an Information Utility - mainly to prevent disputes surrounding debt information. We established the need for this in the first post (and above) when we analyzed the Information Problem.

The sixth objective listed above seems to describe a benefit that the Information Utility process provides - and is not necessarily a core objective.

The second, third, fourth and fifth objectives listed, on the other hand, actually seem to describe the functions of an Information Utility.

Let’s examine what each objective means - and whether fulfilment of this objective would help solve the Information Problem in the Insolvency Process.

An Information Utility serves as a credit and contract repository

What this means

A “repository” is defined as “a place where or receptacle in which things are or may be stored”. So, first and foremost, an Information Utility is a place where credit and contract information are stored.

How this contributes to solving the Information Problem

In our previous post, we discussed how the execution process for loan documents and the storage/updation of debt information over the course of a debt are fundamentally non-neutral.

The original copy of a loan agreement is usually stored with the creditor - and the counterparty with the borrower. The credit information - tallies of repayments and defaults - is also maintained on a system maintained by the creditor.

This lack of neutrality is exploited by borrowers to cast doubt on the integrity and authenticity of debt documentation and information during insolvency proceedings - leading the insolvency proceedings down a rabbit hole of examining and analysing specific documentation. When faced with these aspersions - the NCLT is forced to conduct an examination of the documentation. This process - often involving production of more documentation by either party - causing more delay.

Now, with the Information Utility acting as a neutral entity for storage of debt documentation and updating of credit information. - the NCLT doesn’t need to conduct an examination of documentation or credit information. It can now rely directly on the information stored by the neutral entity - the Information Utility.

This makes it extremely difficult (bordering on impossible) for borrowers to prolong proceedings by casting doubt on the integrity or authenticity of evidence.

An Information Utility accepts financial information from financial or operational creditors or debtors

What this means

Sub-section (2) of Section 13 of the IBC defines 'financial information' as one or more of the following:

- records of the debt of the person;

- records of liabilities when the person is solvent;

- records of assets of person over which security interest has been created;

- records, if any, of instances of default by the person against any debt;

- records of the balance sheet and cash-flow statements of the person; and

- such other information as may be specified.

In most, if not all, cases of financial credit - especially for higher ticket loans - the above information is recorded in the debt documentation.

Given that the IU acts as a neutral repository for credit and contract - it almost seems like a truism that it would need to accept the “financial information” mentioned above.

How this solves the Information Problem

Quite frankly - this by itself - does not add anything. Accepting financial information is the basic requirement that an IU must follow if it is to act as a neutral repository of credit and contract information.

Financial information will be authenticated by all the parties of the debt and stored for use as evidence in any legal process - via an Information Utility

What this means

A repository is only as good as the information that is fed into it.

Suppose an Information Utility receives:

- Shoddily executed debt documentation

- Random, unsubstantiated debt information

Its neutrality as a repository would not mean much in the above case! That’s why an Information Utility also acts as an authentication platform for financial information.

NeSL’s authentication platform is known as the Digital Document Execution or DDE platform. The DDDE platform provides a standardised, digital way for:

- eSign of loan documentation

- 100% digital stamping of loan contracts

- Collection of financial information from the borrower

- Submission of financial information and debt documentation to NeSL’s Information Utility Repository for storage

How does this solve the information problem

The Information Utility’s authentication function helps solve the information problem in 3 ways

- Neutral process -

As mentioned above, neutrality of process is extremely critical to minimize disputes. By providing a platform to perform authentication - an Information Utility ensures that neutrality is maintained at each stage - from authentication of debt contracts and information to storage.The NCLT no longer needs to listen to claims made by either party regarding debt information - and can instead simply consult the neutral authority of the Information Utility for accurate information.

- Minimizes errors and mistakes

In our last post, we analyzed how a physical execution process - with multiple touchpoints - has inherent vulnerabilities that cause errors, mistakes and more. A standardized digital system adds capabilities that can greatly reduce these errors.

For instance - direct population of an agreement from a Bank’s Information Management System will eliminate manual filling up errors and blank form signing. Similarly - the digital signing process will eliminate “missed signatures”.

- Removes discretion to take shortcuts

As discussed before, the time consuming nature of the physical execution process is directly at odds with the desire of both the creditor and the borrower at the time of loan disbursal - they both want the loan as fast as possible! This incentivizes shortcuts in the execution process - which leads to “doubts” in the chain of custody of evidence.

In a digital process - execution becomes a convenient process that gets done in minutes - in sync with the needs of all parties involved at the time of disbursal. Further a standardized digital system makes it possible to include steps that cannot be circumvented.

Even if parties want to take shortcuts - they can’t because the system will not proceed with authentication unless all steps have been complied with!

An Information Utility is designed as a two-way communication tool between creditors and debtors for submission and authentication with recording of disputes

What this means

The debt process involves a lot of communication between parties - to coordinate disbursal and terms, to renegotiate and revise arrangements during the course of the debt, to raise disputes etc.

An Information Utility provides a common digital platform for conducting such communication.

How this helps solve the Information Problem

In a conventional flow this communication is conducted on disparate channels - phone, in-person, email, letters/notices. This creates more documentation to be produced as evidence AND adds even more vulnerability into an already vulnerable system. Debtors can exploit this by using revisions to question evidence of default and sowing seeds of doubt.

The IU’s common platform helps by providing a common hub for recording such communication. While actual communication may still be disparate - an IU ensures that this is recorded on a common platform.

This makes it very difficult for a debtor to make after-thought claims during insolvency proceedings - because the NCLT can access the entire unimpeached chain of communication between the parties through the IU.

Do Information Utilities result in faster insolvency proceedings?

Based on the functions it performs - an IU definitely does seem to have the ingredients to solve for the Information Problem in insolvency, minimize disputes related to debt documentation - and help the insolvency process complete in a time-bound manner.

However given the relative novelty of the system - we need to wait a bit longer to see how it plays out on the ground.

Speaking of “on the ground”. Are financial creditors actually using the IU system? Is the IU system mandatory for all creditors under the IBC?

We’ll cover these questions in the next post.

---------------------------------------------------------------------------------------------------------------------------------------------------

In our next post, we cover the legal framework underpinning the IU system - and investigate if the IU system is mandatory for creditors under the IBC.

If you have any questions, feedback or comments - don't hesitate to email the author at aditya@leegality.com

If you're a Bank or NBFC interested in implementing NeSL in a fast and easy way - click on the link in the blue bar below!

.avif)

.avif)

%20(1).avif)